by

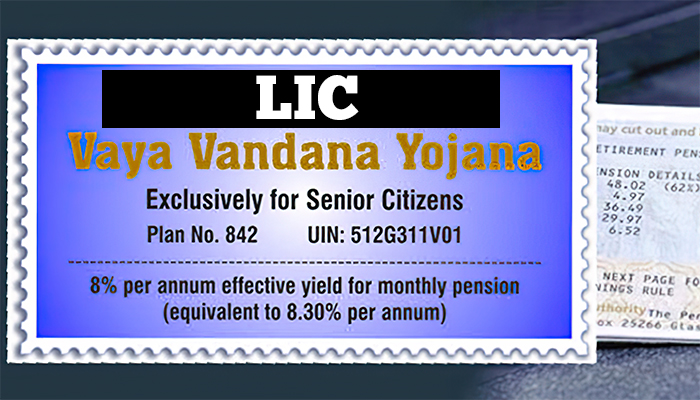

by After the Finance Ministry instructions, the LIC (Life Corporation of India) has extended the validity of Senior Citizens Pension Scheme (aged 60 and above) namely Pradhan Mantri Vaya Vandana Yojana by 3 years i.e. by March 31, 2023. The pension scheme was earlier valid till March 31, 2020 which is now extended by three financial years and is open for investment from 26th May, 2020. Life insurance Corporation of India has been provided the solitary license to operate this scheme.

Under the revised scheme, an assured return of 7.40% per year will be payable on the monthly basis for the entire tenure of 10 years. PMVVY is a non-linked and non-participating pension plan specifically available for the senior citizens and the minimum & maximum pension which can be drawn is ₹ 1,000 and ₹ 10,000 depending on the amount invested in the scheme.

Table of Contents

How to Invest in the Vaya Vandana Yojana?

The scheme is exclusively offered by the LIC of India and only the eligible person i.e. senior citizens aged 60 years (completed) or above can invest in the scheme either through online portal of LIC or by visiting nearest LIC branch.

Link for Online Purchase/Investment -> https://onlinesales.licindia.in/eSales/liconline

The maximum permissible limit in the extended period of three years shall not exceed ₹ 15 lakhs including the previously invested amount, if any.

Interest Rate

For the year 2020-21, the interest rate is 7.40% but for the next two financial years i.e. 2021-22 and 2022-23, the applicable assured interest rate shall be reviewed and decided on 1st April of each financial year by government.

The annual revised rate of interest shall be same under Senior Citizens Saving Scheme (SCSS) upto a ceiling of 7.75 percent with fresh appraisal of the scheme on breach of this threshold at any point.

Read: 7.75% RBI Bonds (GOI Bonds) Features and Taxability

Benefits of PMVVY Scheme

1. Pension Amount

Pension Amount payable as per the chosen pension plan shall be payable through the selected payment mode.

2. Death Benefits

On the death of the pensioner during the tenure of 10 years, the purchase price shall be refunded to the beneficiary/legal heirs.

3. Maturity Benefits

On survival of the pensioner throughout the tenure of 10 years, purchase price along with the final pension amount shall be payable on the last payment date.

Surrender Value

Premature exit from Vaya Vandana Yojana is also allowed but only under the exceptional circumstances such as any medical emergency of self or spouse. The surrender value in this cases shall be 98% of the purchase price i.e. 2% premature penalty shall be levied.

Mode of Payment

The pension payment shall be made through the NEFT or aadhar enabled payment system. The first payment of the pension shall be according to the chosen pension plan i.e. monthly, quarterly, half-yearly or yearly respectively.

Loan

Loan up to the 75 percent of the purchase price shall be granted but only after completion of the 3 years from the year of purchase.

The rate of interest on the loan amount shall be determined on regular intervals. Further, loan amount shall be adjusted from the pension amount and the outstanding loan at the end of the tenure of 10 years shall be adjusted from the maturity proceeds or at the time of surrender.

Free-Look Period

In case the investor is not satisfied with the terms and conditions of the pension plan and would like to surrender the same. He/she can return the policy in Free-Look Period i.e. within 15 days (30 days if this policy is purchased online) from the date of receipt of the policy stating the reason of objections.

The refund shall be granted after deducting the stamp duty charges and pension paid, if any.

Capping of Management and Operating Expenses

For the first year of the tenure, management expenses shall not exceed 0.50% p.a. and for the rest 9 years of tenure, the maximum expenses towards management and expenses shall not exceed 0.30% p.a.

Medical

No Medical Examination is required under the PM Vaya Vandana Yojana Scheme.

Taxes on PM Vaya Vandana Yojana

The amount of pension received shall be taxable as per the applicable tax rate. The pension is to be treated as the salary income and taxed accordingly.

Exclusion

Full purchase price shall be paid in case of death of the pensioner is even due to suicide.